An Energy Tariff Deficit Fund would help people through the crisis and tackle inflation

Ofgem’s October price cap announcement, due on 26th August, is expected to be almost three times the cost versus the same time last year, and January will be even higher

Some government support for households exists but much more is needed

We’re working relentlessly to try and ensure more support is in place for customers

Working with other suppliers, we're proposing an energy tariff deficit fund be put in place before October

This fund would allow prices to be capped at their current level of £1,971 (or slightly higher) before reducing over time

This intervention would also be anti-inflationary, eliminating further increases in customer bills - with wider benefits for cost of living and keeping interest rates down

What should be done about rising energy bills?

The energy price cap from the 1st October will be announced later this month. It’s likely to be around £3,500 for a typical home – 2.7 times higher than the same time last year (with price rises being driven by the global gas crisis). By January prices will be dramatically higher again. This is simply untenable for most households.

While the government announced the Energy Bill Support Scheme and other measures back in May, these will not be enough to support customers with the price rises expected this winter. Octopus is working alongside other suppliers to find solutions. An Energy Tariff Deficit Fund is one such solution that could be quickly implemented to stop the further increases anticipated.

Octopus backs an 'Energy Tariff Deficit Fund'

An Energy Tariff Deficit Fund, implemented prior to October price cap increases, would allow customer bills to be held at or around their current level of £1,971 for the next 3 years and decreased after that down to £1,100 over a decade.

The fund would help smooth prices, sheltering customers from the worst of the global gas prices for the next 3 years whilst they’re still high by freezing tariffs at or around their current level. After that, we’d expect wholesale energy prices to come down through a combination of the end of the gas crisis, a roll out of cheaper renewable generation and changes to the way power is priced. Then, over the next ten years, customers’ bills could come down – priced so that the fund could be paid back in parallel with passing savings through to households.

It’s worth noting that there are various ways this could be repaid. Our modelling is done based on paying this back through energy bills, but the government and regulators could choose to pay this back in a variety of ways:

Pay back as energy prices drop below capped levels - as described here

Pay back via general taxation

Pay back through windfall taxes on companies which have made extreme profits in this period

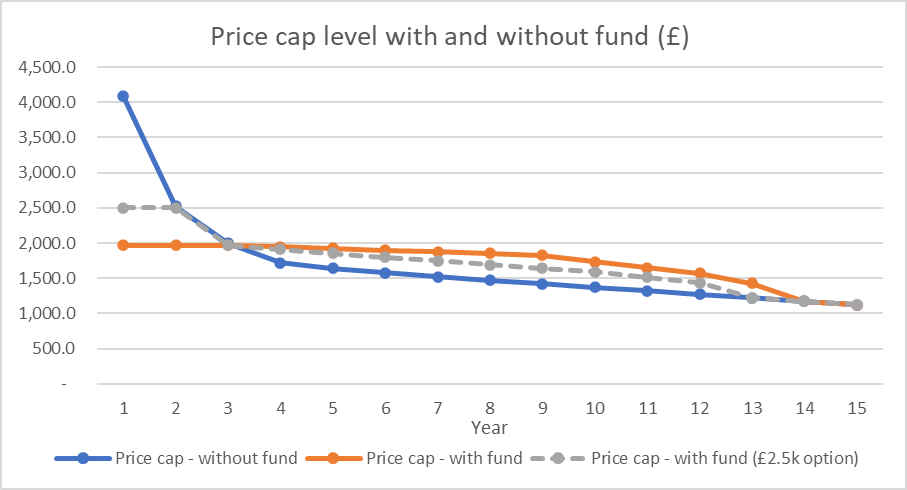

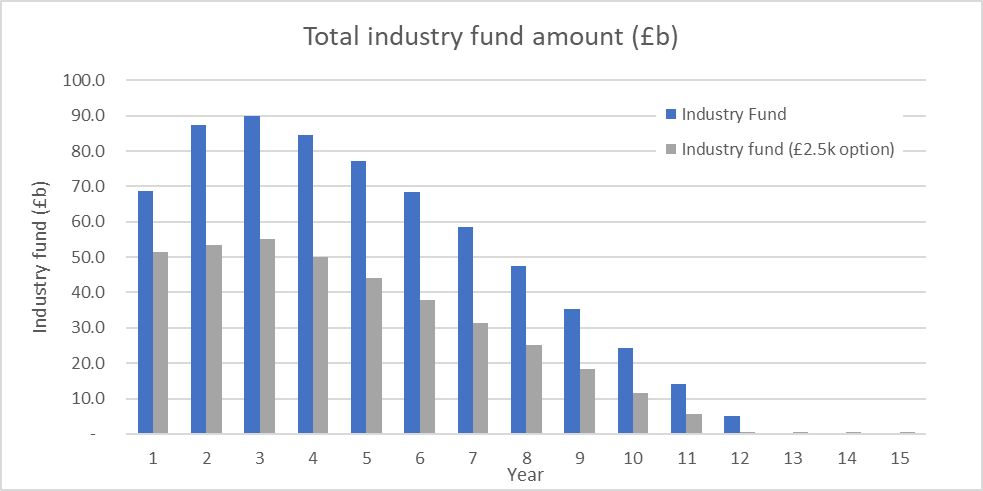

Our modelling shows that following approach 1 above, the total fund would peak at £55-90bn in 3 years depending on pricing decisions made (equivalent to c£2,000-3,000/household) and this could then be repaid over the subsequent 10 years whilst in parallel reducing bills - see figures 1 and 2.

Figure 1: Blue line - forecast price cap level per year starting from Oct-2022 without a fund. Orange line - price cap level with an industry fund with no further price cap increase versus today. Grey dotted line - price cap level with an industry fund and some further price cap increase versus today.

Figure 2: Total fund amount based on costs and prices from Figure 1. Fund peaks at between £55-90bn after year 3 before coming down over the next decade depending on pricing decisions made.

In our modelling, we have assumed that the price cap level over the next 12 months would be £4,086, with wholesale prices of >£500/MWh and >400p/therm. After this, we assume wholesale prices drop down over 5 years to £81/MWh, and 123p/therm (still higher than they were before the crisis but much lower than today) and thereafter slowly return down to pre crisis levels reflective of the underlying cost of producing energy.

These models are based on predictions about what energy prices will be over the next few years - there’s no guarantee that’s exactly right, so we’ve run a range of scenarios of different wholesale forecasts and price cap levels. An energy tariff deficit fund is flexible and works in all these cases. If you'd like more information, do get in touch.

What happens if energy prices don’t come down?

Fundamentally the cost of producing most forms of energy hasn’t changed - what has changed is the price to buy it. That’s why we are seeing oil and gas companies making such enormous profits.

Over the long term that can’t be sustained and prices will come down to be reflective of the cost of producing energy. The question is when will they.

We’ve run various scenarios and a tariff deficit fund works in all these cases - but in ones where prices stay higher for longer, it will take longer to drop customer prices from their current level - and they may even need to be slightly higher. Even in this case customers are massively better off than if prices are allowed to increase to £3,500 or higher in October.

Is this better than allowing bills to rise now, perhaps with targeted support for those who need it most?

This approach has four key advantages:

It directly tackles inflation - reducing contagion from fuel into the wider economy. Targeted support cannot do that.

The rises are huge. By January, bills could be 4-5 times higher than 2020/21. For households on the typical incomes, fuel costs will have risen from about 5% of their post-tax income to 20%. Targeting simply doesn’t work when middle-income households are affected to this degree

Spreading the cost at a low cost of capital nationally is dramatically cheaper than households individually borrowing to get through the crisis

The wholesale market is so volatile that “chasing” these costs with targeted support is simply not possible

Even though some objections are raised on the grounds of “costs need to be passed on to drive efficiency and behaviour change” - the reality is that even freezing bills as they are now, they would be 50-80% higher than usual.

Some object to universal support on the grounds that it shouldn’t be provided to those who don’t need it. In its purest sense, a fund is equally funded by, and benefited from, proportional to usage, so this objection does not hold.

Similarly - the question may be asked - is it right for such a large fund to be introduced, with its long-term commitment. Simply - the energy sector already has many such mechanisms and commitments - it’s the way we pay for grid enhancement, nuclear power stations and much more. Here, it’s paying for the consequences of war.

Published on

Hamish Lazell

Strategy Manager