Locational pricing: our response to the government's REMA consultation

Want to understand more about zonal (locational) pricing? Read our introductory blog: Zonal pricing explained.

Read on for our response to the government's REMA consultation.

A summary of the key points in our response to the Government’s most recent consultation on the Review of Electricity Market Arrangements (REMA).

REMA is exploring the wholesale and investment support reforms required to reach Net Zero.

In short:

The power system is undergoing transformation - demand and many thousands of flexible low carbon assets all over the country can now play a vital role in operating a renewable electricity system at lower cost. Assets like batteries on the grid or in electric vehicles, and interconnectors, can lower system costs and make better use of renewable power by using green electrons when they are plentiful and cheap (and might otherwise need to be paid to turn off) and injecting stored power or avoiding consumption when there is no wind or sun. This is a 180-degree turn from the arrangements today where the needs of electricity users are met mainly by turning fossil fuel generation up or down.

The single wholesale price across GB often gives the wrong price signal to low carbon flexible assets. This means these assets are doing the wrong thing (worsening network constraints) for the system around 30% of the time. The sooner we correct this, the sooner we can realise savings in cost and carbon from effective use of these assets.

Building more grid is vital but not sufficient to reach net zero - it needs to be accompanied by zonal pricing. It is essential to ramp up network build, but investment is behind schedule, meaning that a better market which makes the most of low carbon flexible assets is more important than ever.

A series of evolutionary reforms to the current single national wholesale market will not be sufficient to address the scale of the challenge ahead, and could harm public support for net zero if constraint payments continue to plaster the headlines. Piecemeal reform will take years and add to investor uncertainty.

Once zonal pricing is in place, it will provide a strong foundation, allowing lighter touch and less distortive renewable and reliability support to be layered on top.

Zonal pricing has been forecast to save the average household just under £600 over the full 16 year modelled period - but savings could be even higher the more flexible a consumer can be with their consumption!

The power system is undergoing a metamorphosis

The power system is not undergoing slow and incremental evolution, it is undergoing a metamorphosis. At the start of this century, a small number of large fossil fuel plants dominated. But we have since seen rapid change: coal stations have retired and renewable energy sources increased from 1% to over 40% of the electricity mix. The system has become more decentralised: the proportion of capacity connected to the distribution network rose from 17% in 2011 to over 50% in 2022 , and more and more connected and controllable consumer devices are being connected each day, with Octopus Energy recently passing 1GW of shiftable electricity capacity in managed EVs alone - enough to power a typical evening in both Leeds and Birmingham combined.

An efficient power system is now one where demand and other flexible assets shift in line with renewable supply, rather than vice versa. Meaning load must turn up and down based on the availability of renewable supply, rather than supply being instructed to turn up and down based on fairly static and predictable demand. Therefore our market design must embed this at its centre to remain resilient throughout the transition.

Transformative change in the makeup of assets, and importantly the loss in inherent flexibility from fossil fuel generation, calls for transformative policy and regulatory change.

REMA presents a valuable opportunity to achieve this. Quick and decisive action is needed so GB can start reaping the benefits ASAP.

The status quo market is not suitable for a transforming power system

Current market arrangements were designed for a system dependent on big generation, not highly distributed flexible demand and other flexible assets for balancing. Most notably the single GB-wide wholesale price is not sufficiently granular to use these resources effectively. Without change the transition will be inefficient, put system resilience at risk and will undermine public support for net zero.

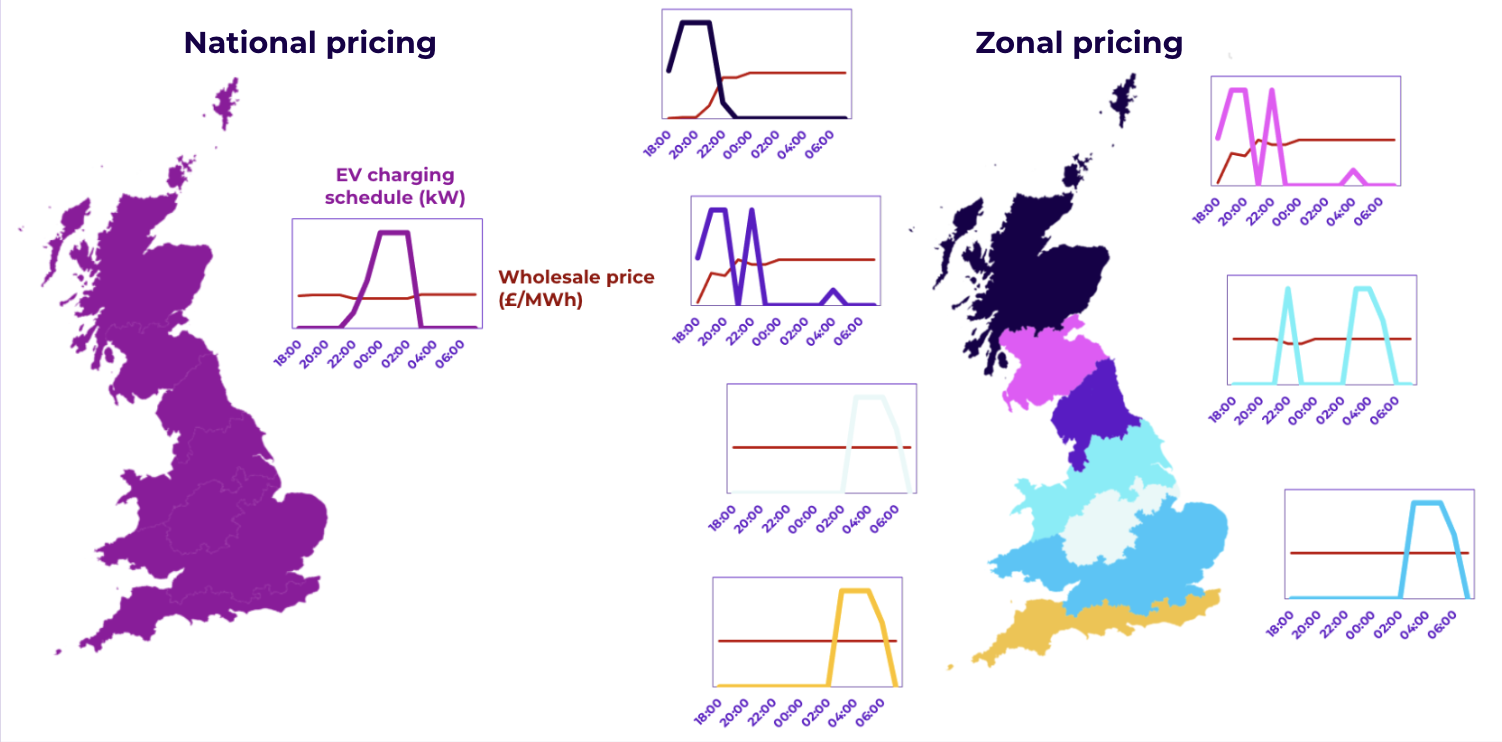

For example, in a given half-hour there may be too much wind generation in one part of the network, but not enough network capacity to take it to another part of the network where it’s needed. Zonal pricing would reflect local supply/demand balance encouraging demand turn up in the zone with wind abundance and turn down in the adjacent zone. These differences in behaviour are not encouraged under a single GB wholesale price, and this is why low carbon flexible assets often operate in ways that increase constraint costs on the system, rather than reduce them.

Figure 1: Shows how EV charging schedules may vary across GB on an example future day (09/03/2030) where wholesale prices differ across zones vs the same schedule sent across GB when there’s only a single GB price

As we invest more heavily in renewable generation, often far from demand centres, the need for stronger regional signals will only grow. REMA must deliver arrangements that not only overcome the challenges of the next few years but provide a pathway towards more enduring arrangements out to 2035, 2050 and beyond. Current arrangements will not maximise the benefits of intelligent demand and low carbon flexibility - essential to successfully rolling out a low cost, low carbon power system that benefits us all. Speed is needed to ensure the right groundwork is laid to enable a swift transition to a fully flexible and renewable-powered system.

Zonal pricing will encourage more efficient balancing, reduce curtailment and provide a hedge against delayed network build

Zonal pricing will reflect losses and network congestion in wholesale prices, giving a price which more accurately reflects the cost of using electricity in a particular location. This more accurate price is fundamental to the effective siting and use of flexible demand and supply assets in line with increasingly variable renewable supply. That’s why it’s key that exposure to zonal prices is not limited to generators but to industrial load, flexible assets and those buying on behalf of consumers. Activation of intelligent demand must be embedded and enabled across all assets able to shift in every settlement period in the year to keep system costs lowest in the future. Alternative reforms which allow opt-in participation are not likely to meet the scale of demand/supply balancing needed in a high renewables power system.

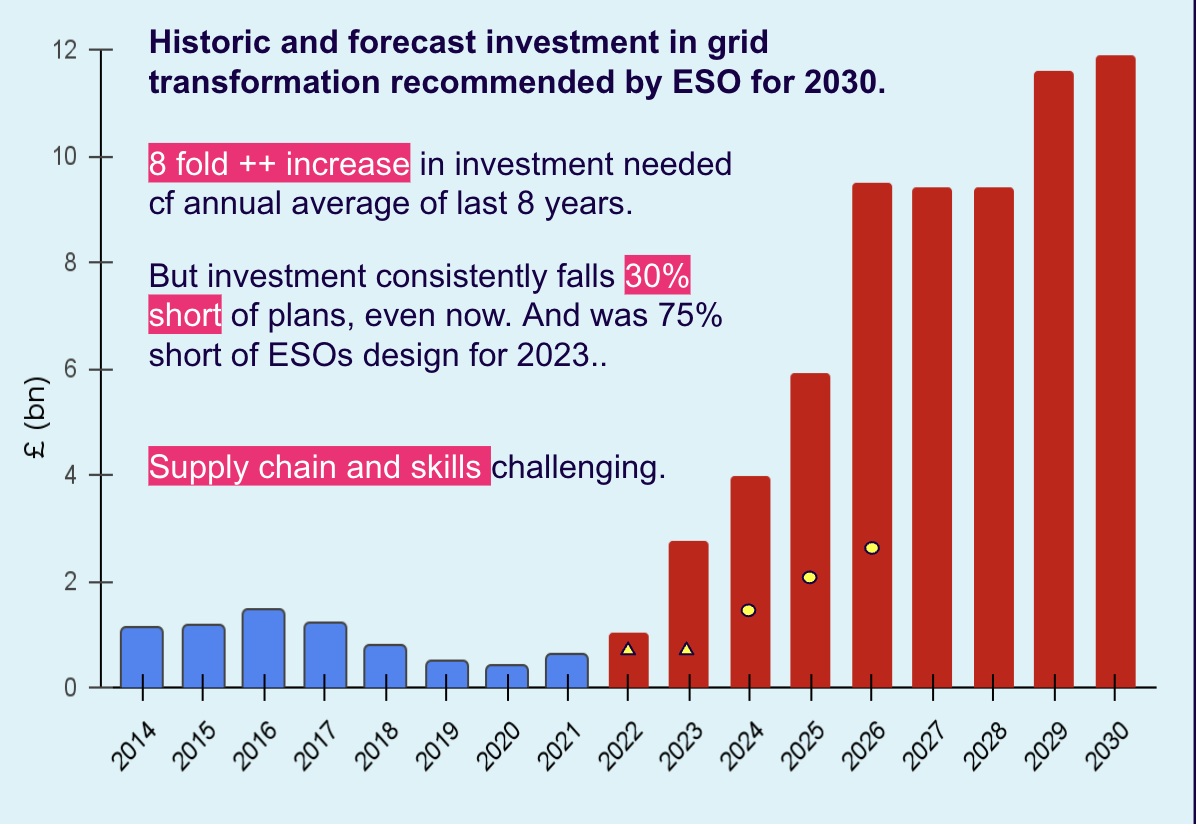

Building more transmission wires to allow more power to reach demand - while fundamental - is not a panacea. Transmission constraints will and should persist as we continue to invest in renewables and despite the expected ramp-up in network build. At present, where transmission constraints exist in a particular area, connected and controllable assets are not directly incentivised to address it through the price of electricity, instead, we pay generation behind the constraint to turn down and generation in front of the constraint to turn up. To realise the benefits of a truly smart and flexible power system, demand must be directly incentivised to turn up and down based on accessible generation output. A build-only approach to the problem will require an 8-fold increase in annual network investment out to 2030 compared to the average spend between 2014-2021, so relying on this alone is a high-risk strategy and will indefinitely lead to spiralling constraint costs.

Figure 2: FTI analysis, showing increase in network investment spend needed to meet 2030 targets vs historic delivered investment.

Alternative reforms to zonal pricing will not work

The past twenty years of incremental market reform (and the ongoing debate on network charging reforms) have not resolved many of the fundamental system issues. Renewable generators continue to locate in areas of oversupply, the system operator takes more and more action close to real time to redispatch the market and flexibility providers make increasingly complex decisions about which markets to participate in to maximise value when ultimately the response requested is near identical across them all.

Years of siloed change processes and a lack of strategic governance have led to ineffective and sometimes even conflicting incentives across different markets. The alternatives to zonal pricing that have been proposed - network charging reform, the rollout of more constraint markets (such as the Local Constraint Market), or changes to how interconnectors are scheduled (reliant on successful EU-GB negotiations) - will not be an exception to this, and even if implemented effectively, they will not go far enough.

Alternative reforms proposed around a single GB wholesale market will be more of the same. They are sticking plaster solutions not fit for the longer-term power system and this fundamental shift in the need for demand to be dispatched according to generation output, rather than the other way around. They will not deliver the operational benefits a zonal market is capable of, will create problems of their own and are likely to lead to higher overall system costs (through increased balancing costs resulting from less well-coordinated markets). Endless alternative reforms will result in a whack-a-mole approach to policy reform, with constant debate and prolonged investor uncertainty.

Incremental reform may seem the easy option and be appealing to some. But REMA is an opportunity to find solutions that are more robust and that the industry will be confident and proud to stand behind when public questions increasingly arise about the cost of getting to net zero.

We need to act quickly to give developers and networks early certainty about the future direction of travel

Key to maximising the benefits that a regional market could achieve is a swift decision on REMA to ensure alignment with other major reform programmes; such as spatial and network plans. Price signals should be used to complement measures like the Strategic Spatial Energy Plan (SSEP) and Centralised Strategic Network Plan (CNSWP) so that siting is encouraged in line with system needs, not against them. We must stop thinking about markets and networks separately.

The more accurate price signals are, the more useful the response is to them and the more efficient the use of existing network capacity. Early decisions about the market design, and the preferred zonal layout, can inform how we prioritise network reinforcement - most welcome in an age of lagging network capacity, where capital and resource deployment are scarce.

Key to the smooth implementation of zonal pricing is clear transitional arrangements which cover all sunk investments - not only CfD-backed generation. This is vital to ensure Britain remains attractive to investors and that investment keeps flowing as market reforms are made. Given the urgency of the climate emergency and the efficiencies that will be gained from a decision soon on GB electricity market design, work on transitional arrangements and detailed zonal implementation should not be held up by the exploration of alternative reforms.

Getting wholesale market signals right will allow us to reduce reliance on out-of-market support schemes

More regionally accurate wholesale prices would reflect real-time system conditions; key to encouraging local balancing of demand with supply and making optimum use of renewable supply therefore reducing our reliance on high-carbon assets. Once a zonal market is embedded, this forms the foundation on which renewable investment and capacity support can be built. We can then think about the right complementary support that respects the incentives this regional wholesale market drives, which should allow much lighter touch and less distortive intervention.

Better prices - that reflect both location and real-time system conditions - will send the best signals for demand and flexibility, strengthening demand elasticity and reducing the need for additional reliability support. However, getting there could take time and if a centralised mechanism for supporting reliability is still preferred, then a reliability option style capacity market is most compatible with zonal pricing and is most market-based. This would better preserve the signals that this new wholesale market is there to encourage, whilst providing stronger delivery incentives that better guarantee response when system stress events are a threat.

Whilst the current CfD design has been very successful in bringing forward investment at scale, the complete shielding of a growing proportion of generation from wholesale prices is increasingly causing problems. Therefore, the current CfD could also be replaced by an auction-derived payment for new renewables based on MW installed, instead of MWh produced. As long as the payment is sufficiently high then investment should keep flowing. This will result in greater exposure of renewable assets to the regional wholesale market and should allow developers more freedom to operate assets how they’d like and provide stronger incentives to locate in areas of highest system value. There could be additional benefits from such a change too - encouraging more diversity in trading behaviours and more innovation in business models for new renewable development.

In summary, to embed a market design which maximises demand-side and wider flexibility participation, we recommend:

A swift decision to implement a defined zonal wholesale market with full generation and load exposure

Setting out comprehensive transitional arrangements at the same point the zonal decision is announced to retain investor confidence and the pipeline of investment into renewable projects

Once the zonal market is embedded, rethinking the right investment and reliability support mechanisms. These should be lighter touch, to minimise the role of centralised mechanisms and strengthen the role of the new regional wholesale market.

Published on

Sam Whitworth

Energy Market Regulation Advisor