We must reform the electricity market to make this the last fossil fuel crisis ever

With all hands on deck to protect customers from rising energy bills and prepare for a tight winter, policy makers could be forgiven for putting long strategic energy reforms on the back burner. But the energy crisis only makes the need to quickly and cheaply reduce the country’s reliance on gas more urgent. Decarbonisation has never been more critical, but the case for significant market reform is now just as much about energy security, and making our system affordable.

The Government’s Review of Electricity Market Arrangements (REMA) provides a golden opportunity to realise these goals. Existing policies have driven an impressive shift to renewables and REMA must accelerate this trend.

Right now, the market has a major blind spot: it doesn’t provide a strong incentive for low-carbon energy 'flexibility'. It’s unlikely to meet its aims until it does. (Learn more about flexibility and why it's so important in this dedicated blog).

Read on to find out how we can ramp up the kind of low carbon flexibility we need through market reform and key supporting policy measures. A secure, affordable and zero-carbon electricity system is so clearly within our reach.

The case for regional pricing in numbers

We currently rely heavily on fossil fuels to match electricity demand with supply; fossil fuels provide 65% of the UK's 'flexible capacity'. This is a huge source of carbon emissions and it's also really expensive.

The UK has a massive 85GW of intermittent offshore wind energy in the pipeline. That's more than eight times the current operational capacity, and we'll need a lot more flexible capacity to 'balance' this energy.

'Low carbon flexibility' is the answer, it's relatively untapped, and could save the UK £16.7bn a year by 2050.

'Regional pricing' will help unlock this flexibility quickly. Initial studies forecast that by 2035, this could have saved households at least £1000.

Why is boosting low carbon flexibility so important?

If we don’t rapidly match our growing renewable generation with a lot more storage and demand-based flexibility, Great Britain will remain dependent on fossil fuels to balance the grid for years to come. Not only does this hurt our energy security, it also adds a lot of unnecessary cost. Low carbon flexibility massively reduces the need for new capital investment and gas peakers: analysis by the Carbon Trust and Imperial College shows that a fully flexible system could cut the cost of reaching net zero by up to £16.7bn a year by 2050. Simply put, the prize is huge and REMA must grasp it.

a fully flexible system could cut the cost of reaching net zero by up to £16.7bn a year by 2050.

The root of the problem lies in the single GB wholesale market. Setting one half hourly price for electricity across the whole country cannot, with any accuracy, signal when and where flexibility is needed, nor reward flexibility according to its value to the system. For example a high GB-wide wholesale price indicates that we should all try to turn down our usage at that time. But there may still be parts of the country where there is a surplus of wind energy behind a transmission constraint and where the system would benefit from customers using or storing power to make the most of those clean electrons.

With this in mind, the current single GB wholesale market provides weak incentives to shift demand, and can often incentivise demand shifting which exacerbates, rather than relieves, local energy constraints. Wholesale prices which better reflect local generation patterns would encourage a more effective response from flexible assets, and invite retailers and others to innovate in ways which are more beneficial for the grid, and for GB.

If the Government’s market review is to be successful it must, above all else, address this failing. New market arrangements need to provide stronger regional signals which facilitate flexibility to help balance an ever-greener grid and provide an affordable way out of fossil fuel dependency. With a reformed market in place, consequential changes to renewable support mechanisms could, and should, be made to keep investment in renewables strong.

How should we expand low carbon flexibility?

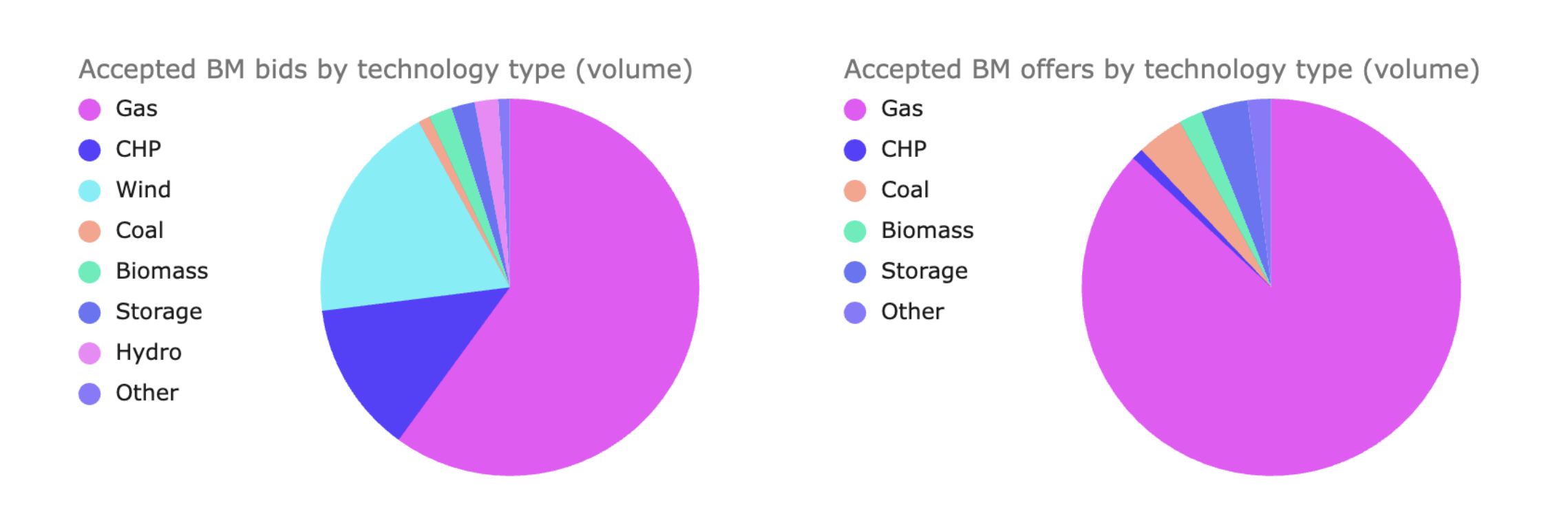

At present, gas still dominates the GB balancing market (ie., how we match energy demand and supply in real time). In 2021, fossil fuels accounted for 65% of electricity system flexibility capacity, with gas providing the vast majority.

Figures 1 & 2: These pie charts show which technologies currently provide flexibility via accepted bid volumes (buying energy by decreasing generation or increasing consumption) and offer volumes (selling energy by increasing generation or decreasing consumption) between 2019 and 2021, sorted by technology, NGESO Markets Roadmap 2022.

There is huge potential to move at pace to replace this capacity with low carbon flexibility afforded by Electric Vehicles, the electrification of heat, and the rapid development of domestic and grid scale batteries. Technological advances mean these low carbon technologies can now be programmed to optimise the support they provide to the electricity system and greatly help reduce emissions at peak consumption periods.

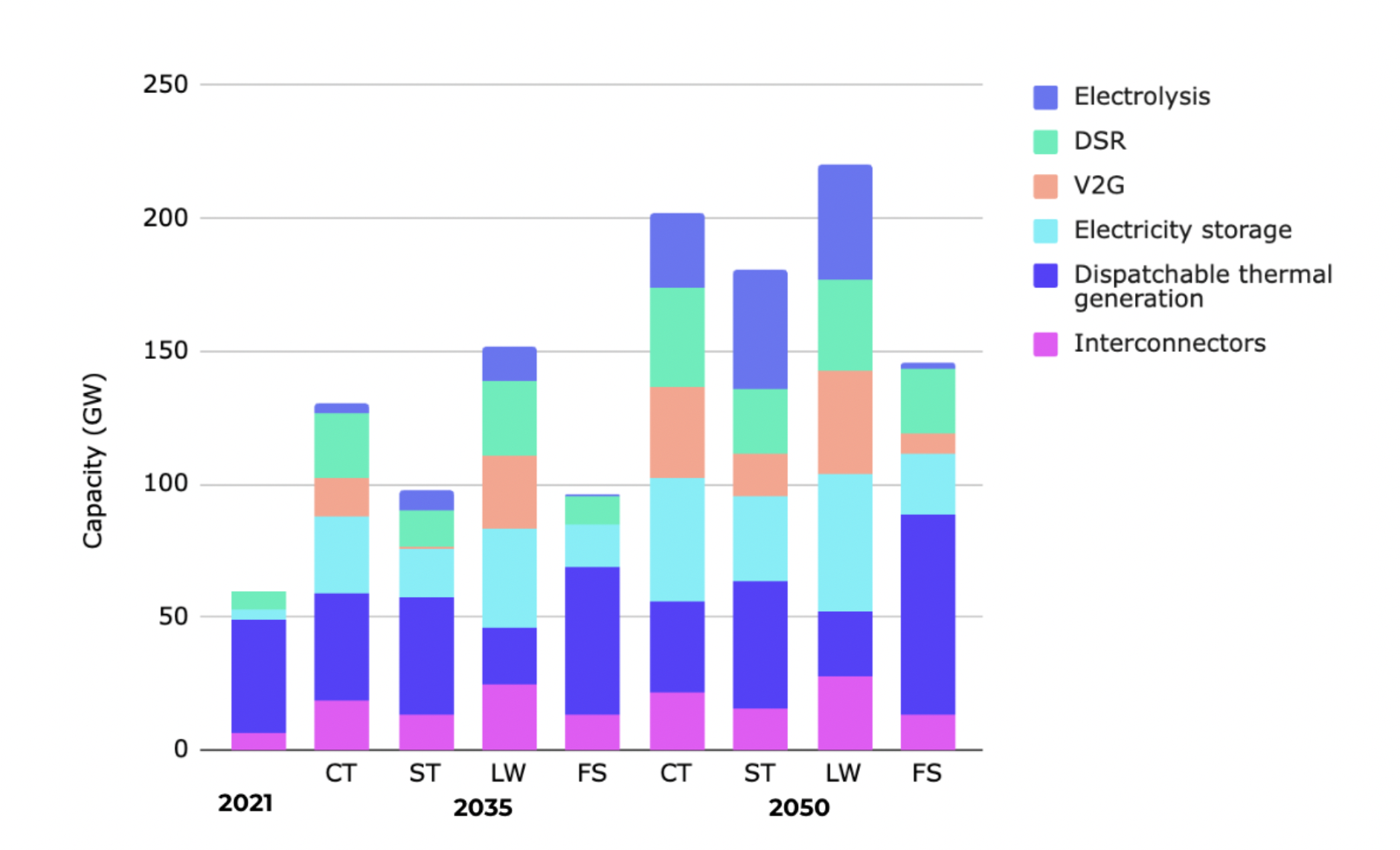

National Grid’s Future Energy Scenarios estimate that by 2035 the system could need more than 15 times more low carbon flexibility than now, and over 20 times more by 2050.

Figure 3: National Grid ESO Future Energy Scenarios 2021 flexibility forecasts. Note that dispatchable thermal generation includes; gas (81%), gas CCS (0%), coal (10%), hydrogen generation (0%), biomass generation (9%), BECCS (0%). Percentages indicate contribution of each technology to 2021 dispatchable thermal generation.

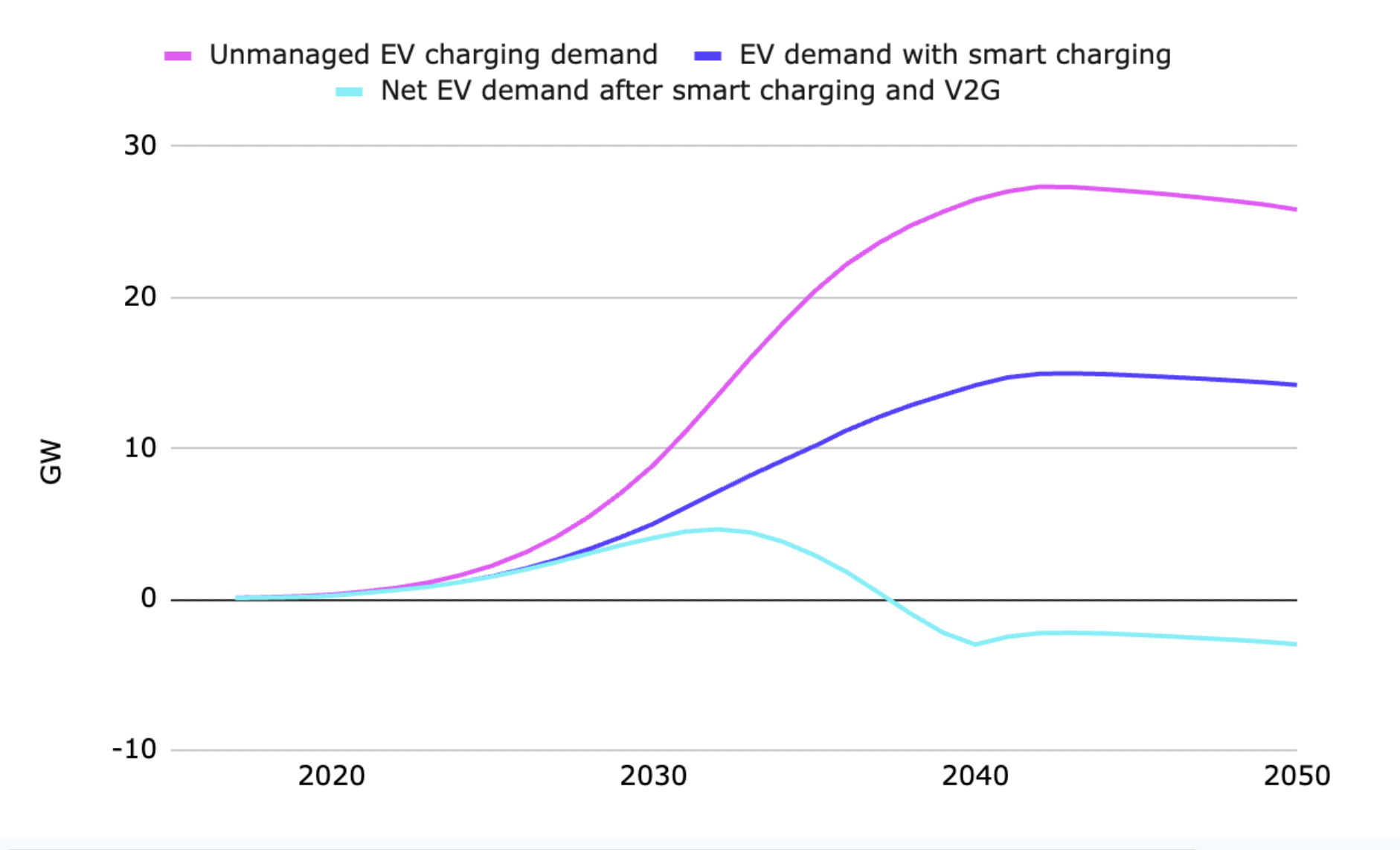

While demand side response is already providing some flexibility, the potential from domestic consumers is relatively untapped. The average EV battery contains sufficient electricity to power a home for 3 days and so provides a valuable source of flexibility. Yet if EV charging is left unmanaged, peak demand could increase significantly, placing significant pressure on local networks and the system as a whole. A compounding impact could be observed from electrifying heating if this too is left unmanaged.

However, smart charging can significantly reduce ‘peaks’ in demand, delaying the need for network upgrades, and even more so if vehicles are able to provide vehicle to grid (V2G) services. (In the same vein, smart scheduling looks set to greatly reduce the impact of low-carbon electrical heating).

Figure 4: National Grid ESO Future Energy Scenarios 2021 Consumer Transformation showing impact on peak demand from EV charging if unmanaged, if paired with smart charging and after smart charging and V2G.

At Octopus Energy, we offer smart tariffs such as Intelligent Octopus which optimise EV charging to the very greenest times. All users have to do is set how much they’d like to charge up and by what time - and we will manage the rest. At the moment, customers on Intelligent Octopus can run their vehicle at just 3p a mile. This is just one example of how it can be made easy for customers to flex their demand, benefit financially and support a low carbon grid.

Regional pricing will harness flexibility - we need to start implementation, fast

While charges for using the energy network already vary across the country, the methodologies to set these charges are relatively inflexible and contain approximations and assumptions which quickly become out of date. They are a blunt instrument, not up to the task of harnessing low carbon flexibility to help balance a zero carbon grid. Reforming the wholesale market to provide dynamic, real time regional prices is a sophisticated, agile way to signal the need for and value of flexibility in different parts of the country, at different times of day. Sharper, more accurate price signals will become increasingly important in the future power system where demand and supply must be better matched to keep costs down. Put differently, a market price that reflects the fundamentals of the system would provide accurate information that reflects the value of different technologies in different areas, and only then can we realise the optimum technology mix needed to balance a decarbonising grid.

The case for ending the single GB market is compelling. We need to move beyond debate and look at how to implement regional pricing. Three things need attention:

Further work is needed to assess whether the new market arrangements should be based on several zones or hundreds of ‘nodes’. In that assessment, the impact of central dispatch on flexibility and demand side response needs particular consideration.

The impact on regional consumer prices - as there is a chance that regional pricing could increase consumer prices in some areas of the country. Analysis which we sponsored, looking at a seven zone model in GB, indicated that consumers in all parts of GB could see a reduction in the cost of their total bill; equivalent to £1000 per household up to 2035. However, even if not, measures can be introduced to limit the variation in prices (if so desired) without destroying the benefits that come with regional markets. This could be done via formal transfers to limit the difference in average prices, or by allowing retailers more discretion on how regional costs are reflected in end user prices, for example.

Renewable support mechanisms, like the CfD regime, must be revised in line with wholesale market reforms, to ensure a continued ramp up of renewable investment and to allow more consumers to benefit from cheap renewable energy. It would also help the investment pipeline if the Government set out transitional arrangements clearly so as to instil confidence and provide early clarity over the direction of travel. The goal must be investment in flexibility and renewable generation - not one at the expense of the other.

None of these challenges are show stoppers when it comes to market reform. It is absolutely vital that we move quickly into implementation mode. A significant volume of renewables are expected to connect to the system in the coming years. 6.3 GW of onshore wind projects have been granted planning permission already – enough for more than 4 million homes.

On top of that, there’s potentially a further 85 GW of offshore wind in the pipeline combining existing projects with ongoing leasing rounds (Aurora Energy Research) – enough for 60 million homes. New market arrangements are needed as soon as possible if we are to ensure that the growth of low carbon flexibility matches the pace of GB’s variable generation - and minimise the otherwise massive costs of that transition.

Dynamic pricing for distribution network congestion should be part of the package

‘Nodal’ or ‘zonal’ pricing that reflects the actual situation on the transmission network will take us a long way to unlocking the potential of low carbon flexibility. But to release the full value we also need new arrangements at the distribution level - where the vast majority of the accelerating stock of Low Carbon Technologies (LCTs) - like EVs and heat pumps - connect.

These smart technologies need price signals to discourage peak consumption in congested areas, but rolling out regional markets on the distribution level (rather than on a wider transmission level) won’t be possible within foreseeable timelines. Alongside a new wholesale electricity market, attention must be given to providing dynamic signals at the distribution level so that smart technologies can play a bigger role in reducing local network constraints.

A flexible system needs a vibrant retail market to encourage and empower customers

For new wholesale market arrangements to be successful, retailers and intermediaries must be encouraged to innovate and develop new products that make it easy for customers to adopt low-carbon technologies and benefit from shifting their energy consumption to times when the grid is less strained and energy is cheaper (and generally greener). In the face of current volatile wholesale market conditions and the trend towards tighter regulation following several retailer failures, innovation and competition in the retail market faces significant risk.

As policy makers look beyond the energy crisis, creating a financially resilient, thriving retail market - and restoring competition - is vital to ensure maximum realisation of benefits from these new wholesale market arrangements.

Ultimately this isn't just about creating a new retail market. This is about moving towards a system where customers aren't afterthought at the end of the grid's cables and wires; a system where customers play a pivotal role in supporting the energy transition - where retailers can give them the tools to decarbonise their energy supply, cheaply and easily.

Published on

Rachel Fletcher

Group Director of Policy and Regulation